A lot of the Small and Medium Enterprises (SMEs) think that they owned all the companies and why does transfer pricing matter to them?

Yes, it does matter. Why? Because the Inland Revenue Board (“IRB”) do not see the Group as ‘One Company’.

As you are aware, budget 2021 has finally passed in the parliament on 16 December 2020 and the particulars in relation to the TP are the penalty for non-compliance as follows:

- Penalty for failure to furnish Transfer Pricing (“TP”) documentation

Effective from 1 January 2021, with the new inserted subsection 113B(1) of Income Tax Act (“ITA”), on conviction, a penalty of RM20,000 to RM100,000 or imprisonment up to 6 months or both, if the taxpayer fails to furnish the TP documentation within 30 days to IRB. - Penalty for a TP adjustment give arises to tax undercharged

Section 140(3C) of ITA provided that regardless of whether the taxpayer is in a taxable or non-taxable position, a surcharge will be imposed. The surcharge shall not be more 5% of TP adjustment of the amount of:- Increase of any income

- Reduction of any deduction

- Reduction of any loss

- What is transfer pricing?

Transfer pricing is the pricing of goods, services and intangibles between related parties.

Related parties are:

a) persons one of whom has control over the other;

b) individuals who are relatives of each other; or

c) persons both of whom are controlled by some other person.

Below are some scenarios of related party transactions.

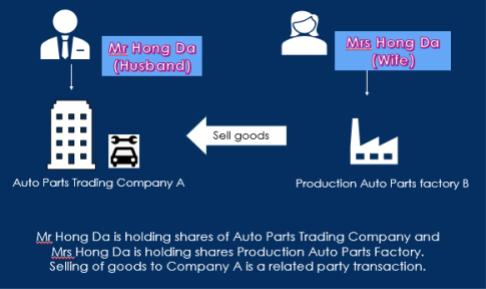

Scenario 1:

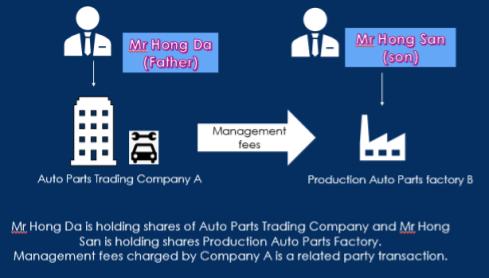

Scenario 2:

Related parties must deal with each other at arm’s length. The arm’s length principle requires that transfer prices between related parties are equivalent to prices that unrelated parties would have charged in the same or similar circumstances. - What is TP documentation?

Transfer pricing documentation should include records and documents describing:- The organizational structure, including an organization chart covering persons involved in a controlled transaction.

- The nature of the business or industry and market conditions.

- The controlled transaction.

- Strategies, assumptions and information regarding factors that influenced the setting of any pricing policies.

- Comparability, functional and risk analysis.

- Selection of the transfer pricing method.

- Application of the transfer pricing method.

- Documents used in developing the transfer pricing analysis.

- Index to documents.

- Any other information, data or document considered relevant by the person to determine an arm’s-length price.

All relevant documentation must be provided in Bahasa Malaysia or English.

- Why you need to have TP documentation?

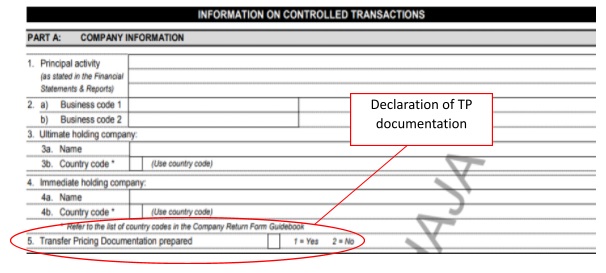

The requirement for declaration of YES or NO in the appendix of Form C.

If a taxpayer does not prepare TP documentation but made a “Yes” declaration in the tax return. The taxpayer is furnishing incorrect particulars in the tax returns and it is an offence under subsection 113(1) of ITA. If the company guilty of the offence shall: - be liable to a fine of not less than RM1,000 and not more than RM10,000 and shall pay a special penalty of double the amount of tax which has been undercharged.

- If no prosecution has been instituted in respect of the incorrect return or incorrect information, the Director General may impose a penalty equal to the amount of the tax which has been undercharged.

- Is your company required to prepare TP documentation?

Yes, once you have related party transactions, you need to prepare a TP documentation to substantiate that your transactions with related party are at arm’s length.

Not sure whether you need to prepare TP documentation? No worry, please do contact us and we will provide a FREE assessment to the company on whether the company is required to prepare a TP documentation.